insider dedicated to your success

with experience from the following companies:

Step 1

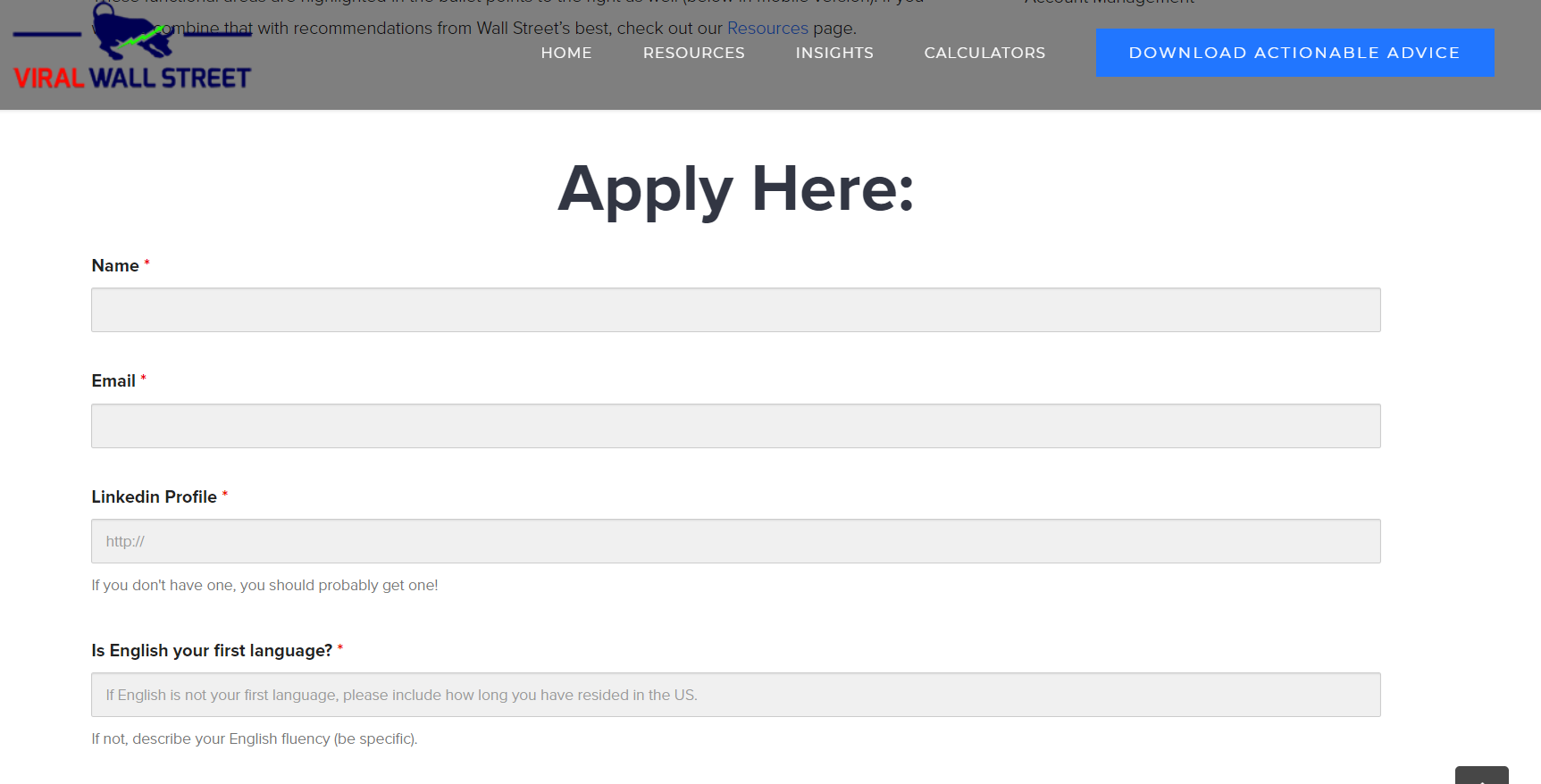

Fill out the application

Fill out the application

Step 2

Match with a mentor who intimately knows your path to success

Step 3

Your mentor will guide you to the right path:

Your mentor will guide you to the right path:

Land on Wall Street